Have you ever had a trade that looked perfect on paper—clean technical setup, solid fundamentals, everything aligned—only to watch it immediately move against you the moment you entered?

Or maybe you've experienced the opposite frustration: identifying a great opportunity but hesitating to pull the trigger, only to watch the stock rocket higher without you.

If you're nodding along, you're definitely not alone. Most traders struggle with the same fundamental challenge: emotion-driven decisions that sabotage otherwise sound analysis.

- The fear of being wrong

- The greed to maximize every move

- The paralysis of having too many variables to consider

These psychological hurdles often matter more than your technical skills or market knowledge.

But what if you could remove emotion from the equation entirely?

What if there was a way to identify high-probability setups, enter and exit at predetermined levels, and let the market's own structural forces work in your favor—all without second-guessing yourself or fighting your instincts?

That's exactly what our PTrans2PGEX mechanical trading strategy delivers.

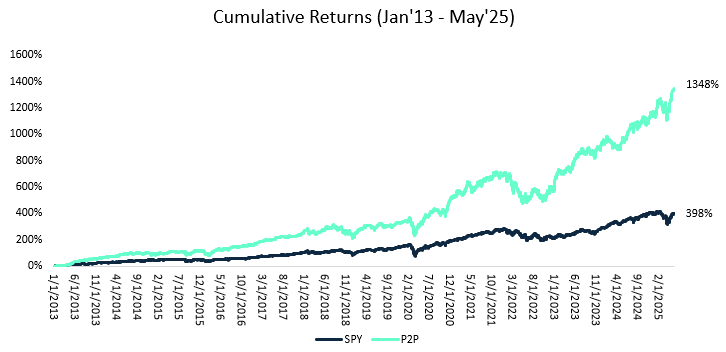

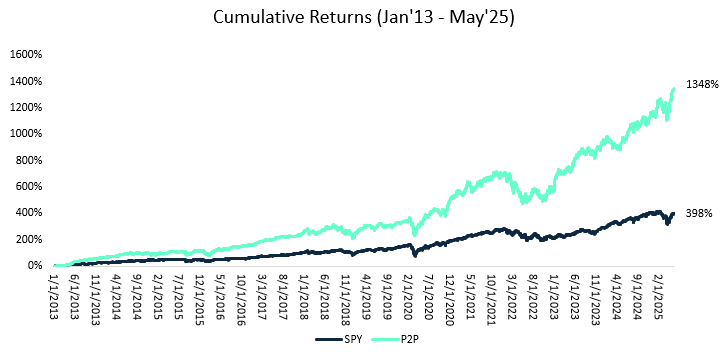

Over the past 12+ years, this systematic approach has generated 1,348% total returns compared to SPY's 398%—nearly 3.4x the performance of simply buying and holding the market.

This isn't about chasing hot stocks or timing perfect entries. It's about understanding how options market structure creates predictable price movements and positioning yourself to benefit from those patterns consistently, trade after trade.

In fact, we've curated a list of those "large cap quality stocks" driven by options markets which we include in our universe of selectable stocks for the strategy. This is called the GammaEdge liquidity list (think AAPL, TSLA, MSFT, META, etc.).

In this lesson, you'll discover:

- The complete backtested performance across multiple market cycles (including recent results that will surprise you)

- The surprisingly simple entry and exit rules that drive these results

- How to implement this strategy using GammaEdge tools in just minutes each day

- Why removing discretion actually improves performance

- How our live portfolio has validated the backtesting in real-time

Ready to see how systematic, emotion-free trading can transform your results? Let's dive into the proof.

And if you'd refer to watch a video of this newsletter rather than read it yourself, no problem! We've prepared a video for you below:

The Proof: Backtested Results

Before we dive into how the strategy works, let's address the elephant in the room: Does this actually deliver the performance we're claiming?

The short answer is yes—and the numbers are even more impressive when you see them broken down across different market environments.

Special thanks to our backtesting partner EdgeRater, whose sophisticated platform enables us to conduct rigorous performance analysis across multiple market cycles.

12+ Year Track Record (January 2013 - May 2025)

Over the last decade plus of various market conditions, the results speak for themselves:

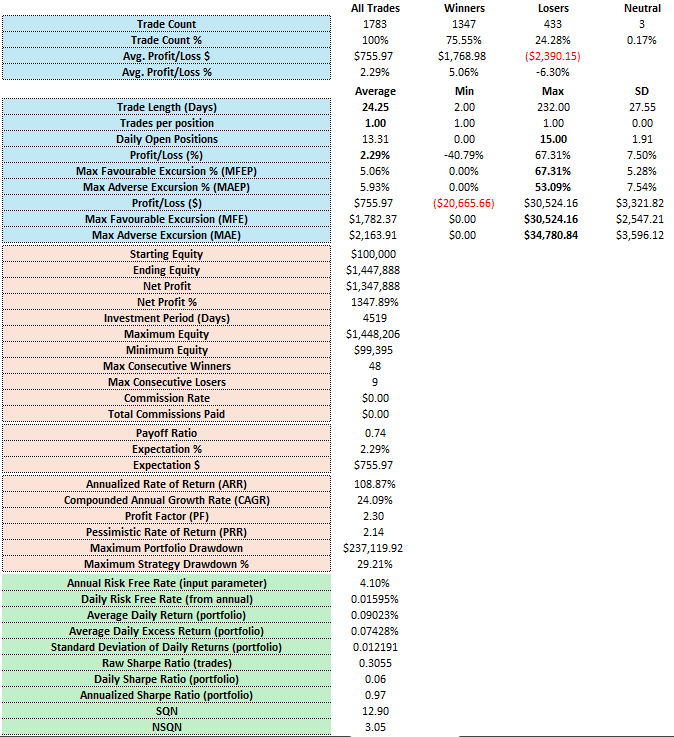

- Total Returns: 1,348% vs SPY's 398%

- Win Rate: 75.55% across 1,783 trades

- Average Trade: $755.97 profit (positive expectancy)

- Maximum Drawdown: 29.21% vs SPY's 33.57%

You experienced less downside risk while generating nearly 10x the absolute returns. This is consistent outperformance through the 2015 taper tantrum, 2018 correction, 2020 COVID crash, and 2022 bear market.

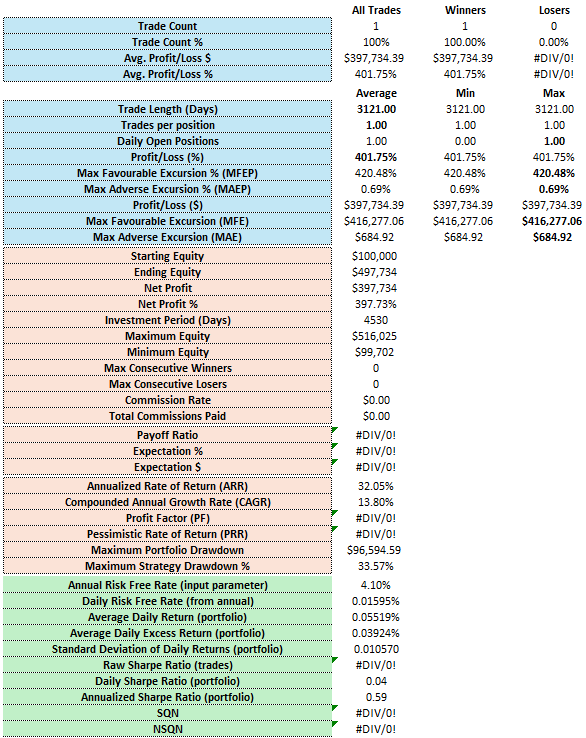

SPY Backtested Stats

P2P Backtested Stats

Equity Curves

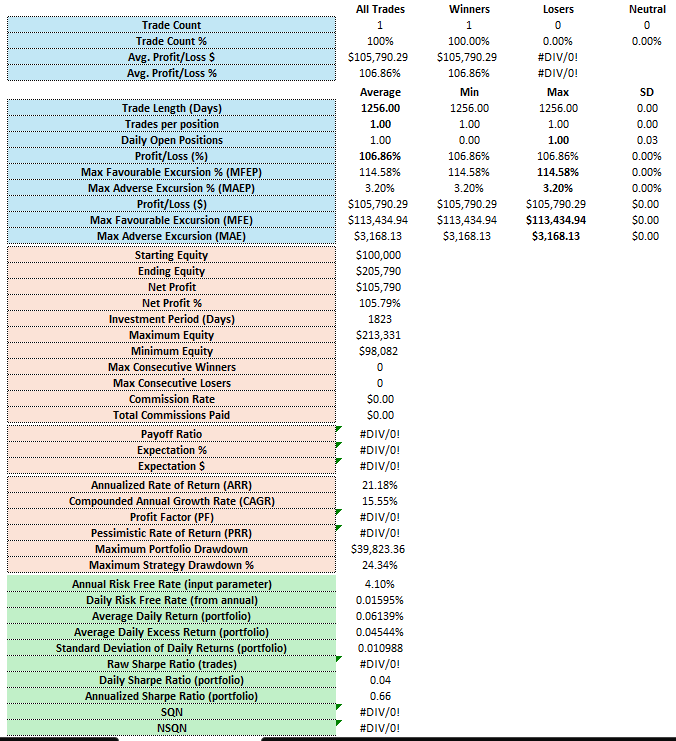

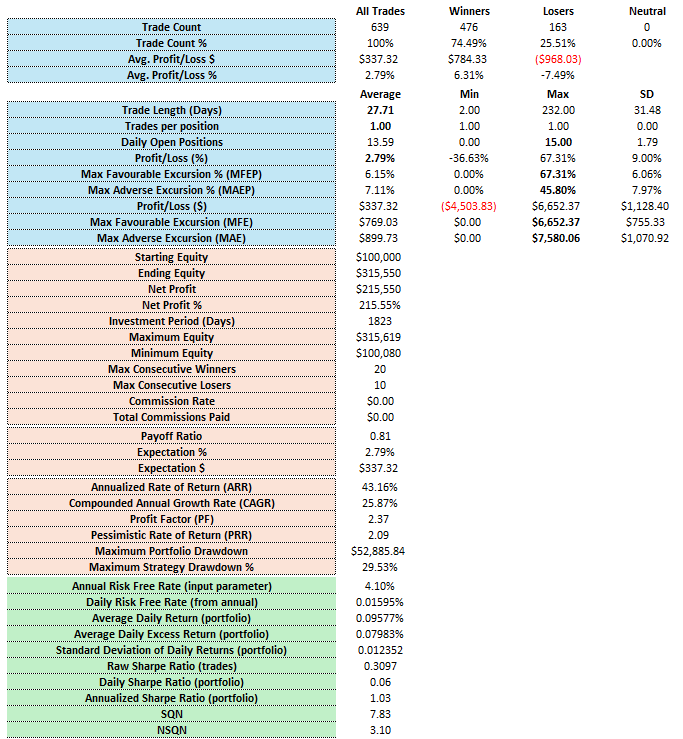

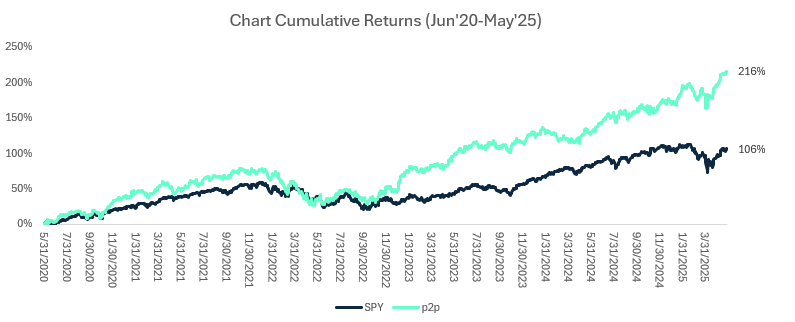

5-Year Performance (June 2020 - May 2025)

The more recent period shows the strategy's adaptability:

- Total Returns: 216% vs SPY's 106%

- Consistent Outperformance: Steady progression through dramatically different market regimes

- Risk Management: Better downside protection during the major corrections

What's particularly compelling here is how PTrans2PGEX maintained its edge through dramatically different market regimes—from the 2020-2021 everything-bubble to the 2022 bear market to the recent AI-driven rallies.

SPY Backtested Stats

P2P Backtested Stats

Equity Curves

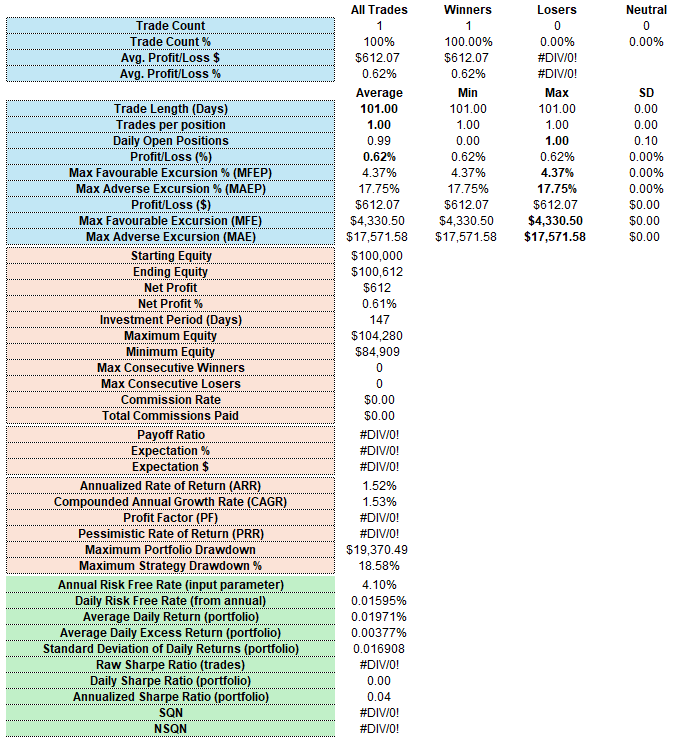

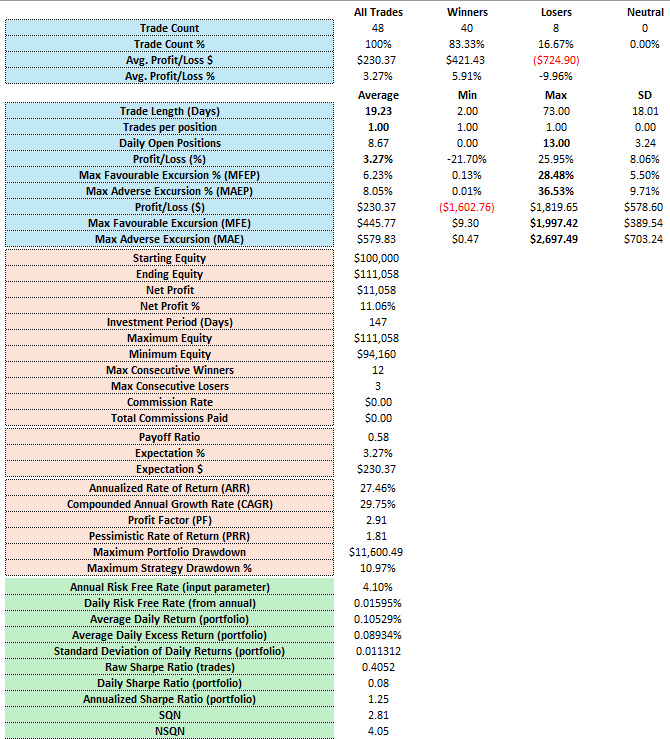

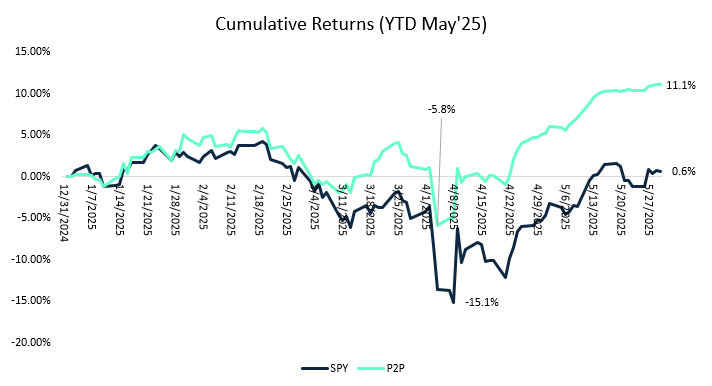

Recent Performance (YTD May 2025): The Real Eye-Opener

This is where the strategy's risk-adjusted performance becomes crystal clear:

- PTrans2PGEX: +11.1% with 10.97% maximum drawdown

- SPY: +0.6% with 18.58% maximum drawdown

While SPY investors endured an 18.6% drawdown just to earn 0.6% for the year, PTrans2PGEX captured 11.1% returns with nearly half the downside risk.

The strategy delivered:

- 83% win rate (40 winners, 8 losers out of 48 trades)

- 27.46% annualized return

- Sharpe ratio of 1.25 (excellent risk-adjusted performance)

SPY Backtested Stats

P2P Backtested Stats

Equity Curves

"But Wait—Is This Just Backtesting?"

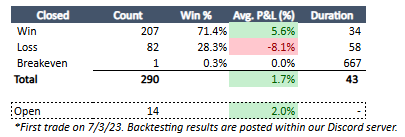

Since July 2023, we've been running this strategy live in our Discord community, posting every entry and exit in real-time. No cherry-picking. No hindsight adjustments. No theoretical performance.

And the forward-testing results have matched the backtesting.

Every trade is documented publicly, tracked in a shared Excel spreadsheet, and discussed openly with our community. You can see exactly how the strategy performs when real money is on the line, complete with the occasional losing trades and drawdown periods.

This isn't some hypothetical system we're selling you—it's a strategy we use ourselves and share transparently with our community.

The strategy works because it's based on structural forces in the options market that create predictable price movements. When those forces align with our entry criteria, we participate. When they don't, we wait.

Simple. Systematic. Profitable.

Bottom line: $100,000 invested in January 2013 would be worth $1.45 million today using PTrans2PGEX, compared to $498,000 with SPY.

And before we move on, here is the link where you can see our trades for yourself: https://1drv.ms/x/c/37a09e23bf750b1a/EZOBBAM8eIlNj1RrNWrHrdgB8OpfLYsK79rM3PeLKFWnTg?e=kkhPth

(output above is as of 05/22/25)

Strategy Background & Core Concept

Now that you've seen the results, let's break down what PTrans2PGEX actually means and why it works so consistently.

How It Works

PTrans2PGEX utilizes two key GammaEdge levels derived straight from options market structure:

- PTrans: Where call speculators take control of the options structure (our entry point)

- PGEX (+GEX): Where the highest concentration of call gamma sits (our profit target)

The Core Insight

In today's markets, options often drive stock prices. When traders buy calls above the current price, market makers must hedge by buying stock. As prices rise toward those strikes, hedging pressure intensifies, creating a feedback loop that accelerates price movement.

Our strategy identifies when this structural setup is in place and positions us to benefit from the resulting acceleration.

PTrans was constructed to identify the threshold where the market structure is dominated by calls. This implies that at this strike price and above, the market expects the price to keep rising. As the price ascends, dealers face increasing directional risk from their short calls (i.e., traders are long OTM calls), compelling them to hedge by buying more shares. This action further drives the price up. Our strategy aims to capitalize on this dealer-induced buying pressure, exploiting the market dynamics for potential upside gains.

+GEX is the natural upside target for this strategy as this is the most convex call strike in the complex. In laymen’s terms, we see the most short-term speculation at this strike. Once this level is reached, those call holders have realized significant appreciation in their options contract. In fact, as this is the maximum point of convexity, their option position will start to increase at a slower rate going forward. In other words, much of the ‘juice has been squeezed’ from their position.

IMPORTANT CLARIFICATION: This strategy involves trading shares of stock, not options contracts. While we use options market structure to identify entry and exit points, all positions are taken in the underlying equity. This makes the strategy accessible to any trader with a standard brokerage account and eliminates the complexity and time decay associated with options trading.

The Rules (Beautifully Simple)

- Entry: Stock starts the current session below PTrans and closes the session above PTrans → Enter occurs at next market open

- Exit: Stock closes the current session above PGEX → Exit at next market open

- Position Sizing: 4-7% of account equity per position

- Stop Loss: None (backtesting shows stops hurt performance)

IMPORTANT NOTE: There is no stop loss employed with this strategy. Through our back testing (which we hit on above), we have found that incorporating a stop loss degrades performance. Despite the lack of a stop loss, there is an exit rule to this strategy, which was just discussed above. This is not to say you will not take heat (i.e., experience a draw down) with this strategy because you will (as we’ll show in the backtesting results). However, as with any strategy, you must stay the course and follow the rules. Position sizing is key for this strategy, so pay attention to this as you review the backtesting results.

Why Mechanical Execution Matters

Discretion usually hurts performance. When you start second-guessing—"This one looks risky" or "Let me wait for a better entry"—you introduce the emotions the system eliminates.

The beauty: Did it close above PTrans after starting below? Enter. Did it close above PGEX? Exit. Everything else is noise.

Implementation with GammaEdge Tools

We've built the entire infrastructure to make PTrans2PGEX implementation almost effortless.

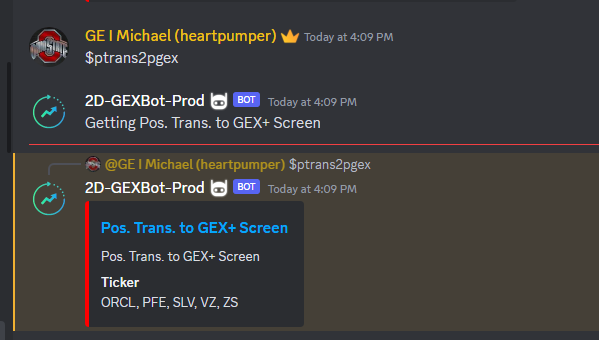

For entry candidates, we have created a scan called $PTrans2PGEX that is available in the discord. Once end of day processing occurs (typically after 5:45 pm EST), you can run the scan below to find valid candidates that can be entered at the opening of the following session. Below is an example of how to execute the command:

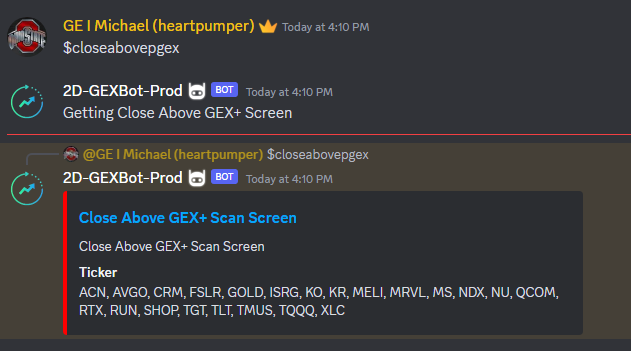

For exit candidates, we have created a scan called $closeabovepgex. Again, once end of day processing occurs (typically after 5:45 pm EST), you can run the scan below to find valid candidates that should be exited at the open of the following session. Below is an example of how to execute the command:

This strategy’s back testing is based on end-of-day data. Therefore, these screens need to be run before 630 am EST, which is when we receive our premarket updates for the upcoming session.

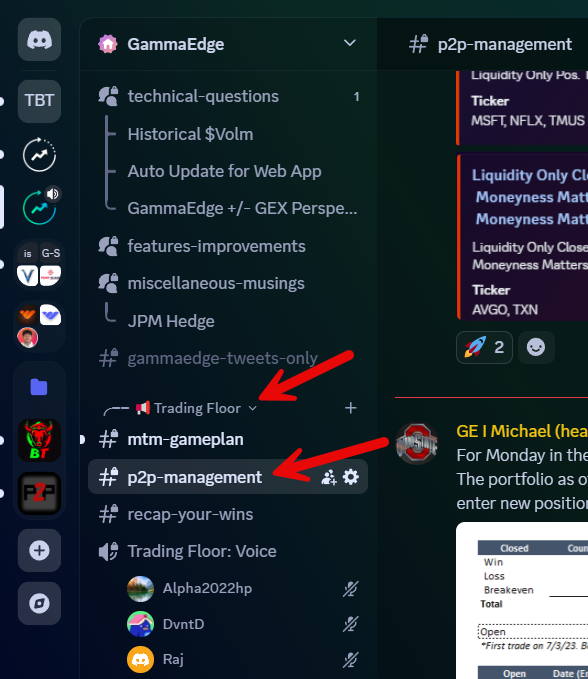

In case you have forgotten to run these scans in that time window (although it’s likely someone else has done this and you can search discord for that scan run), we have created the following channel within discord where the scan outputs are produced for you called #p2p-management. Within this channel, we also include our proposed actions for the upcoming session (i..e, entries and exits).

Your Daily Workflow

After Market Close (5:45-6:00 PM EST):

- Check #p2p-management for scan results

- Note new entries and exits for tomorrow

Market Open:

- Execute entries/exits from previous evening's signals

- Update position tracking

That's it. No intraday monitoring. No second-guessing. No emotional decisions during market hours.

Final Thoughts

By now, you've seen the performance data and understand the mechanics. The question isn't whether PTrans2PGEX works—it's whether you're ready to execute it consistently.

The system only works if you follow it exactly. Take every signal, exit at +GEX, size positions consistently, and trust the process during losing streaks. The 12+ years of data includes all market conditions—your job is to execute and let probabilities work in your favor.

The strategy works. The tools are ready. We track it live in the Discord.The only variable left is your execution.

Until next time,

Taylor

GammaEdge Co-Founder